Flood Zones: The Hidden Cost Most Investors Overlook

FEMA flood insurance can cost $3,000-15,000 per year. Learn how to factor this into your property analysis before making an offer.

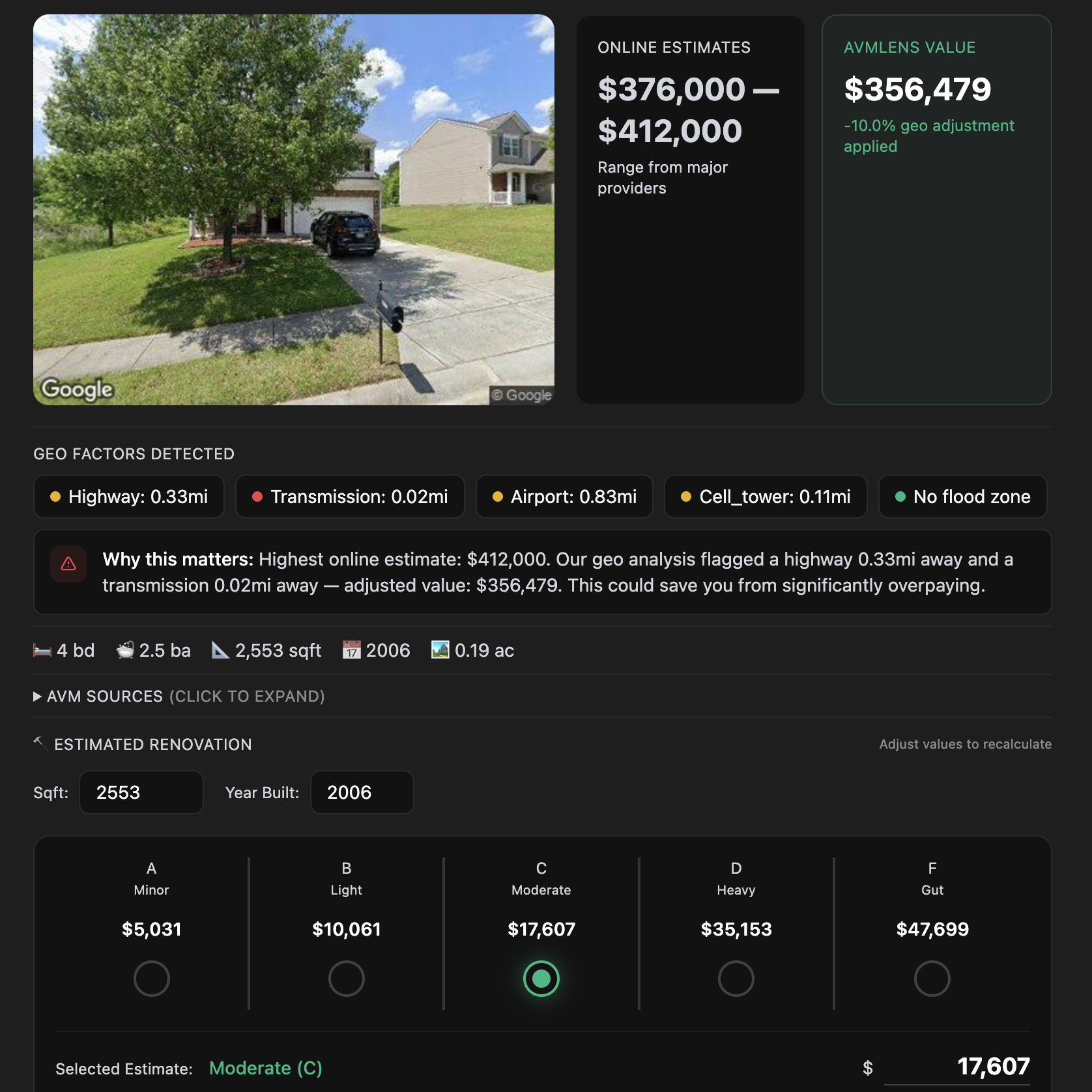

You find what looks like a great deal - a property priced 15% below comparable homes in the area. The AVM says it's worth more. The numbers work. You're ready to make an offer.

Then you discover it's in a FEMA Special Flood Hazard Area. Suddenly, that "deal" isn't looking so good.

Flood insurance in high-risk zones averages $3,000-7,000 per year for a typical single-family home. In coastal areas or repeat-flood zones, premiums can exceed $15,000 annually. This is required if you have a mortgage.

Understanding FEMA Flood Zones

FEMA designates flood risk using a zone classification system. Here's what you need to know:

| Zone | Risk Level | Insurance Required? | Typical Premium |

|---|---|---|---|

| AE, A, AO | High Risk (100-year flood) | Yes (if mortgaged) | $3,000-15,000/yr |

| VE, V | High Risk + Waves | Yes (if mortgaged) | $5,000-20,000/yr |

| X (shaded) | Moderate Risk | No (but recommended) | $400-1,500/yr |

| X (unshaded) | Minimal Risk | No | Optional |

How This Affects Property Values

Let's do the math on that "deal" property:

Property: 3BR/2BA in Zone AE

- Asking price: $340,000 (15% below comps)

- Annual flood insurance: $5,200

- 10-year insurance cost: $52,000

- Present value of insurance (7% discount): ~$36,500

That 15% discount? It's really only ~4% after accounting for insurance costs.

And this assumes premiums stay flat. FEMA's Risk Rating 2.0 system has increased many premiums significantly, and climate change is making flood events more frequent.

What Most AVMs Get Wrong

Traditional AVMs don't factor flood zone status into their valuations. They'll happily tell you a house in Zone AE is worth the same as an identical house in Zone X - even though the Zone AE property has a structural cost disadvantage that will persist for the life of the property.

Smart investors need to adjust AVM values for:

- Capitalized insurance costs: Present value of expected premiums over a typical holding period

- Reduced buyer pool: Cash buyers only won't need insurance, but they'll negotiate knowing future buyers will

- Resale friction: Disclosure requirements mean every future buyer knows the risk

Due Diligence Checklist

Before buying any property, check these flood-related factors:

- Current FEMA zone: Use FEMA's flood map service

- Pending map changes: FEMA regularly updates maps - a Zone X property might become Zone AE

- Elevation certificate: Properties above base flood elevation may qualify for lower premiums

- Flood history: Has the property flooded before? Ask for disclosure.

- Actual insurance quote: Don't estimate - get a real quote from an insurance agent

When Flood Zone Properties Make Sense

This isn't to say you should never buy in flood zones. Some scenarios where it can work:

- Significant discount: 20%+ below comps after insurance capitalization

- Elevated structure: Properties built above base flood elevation have lower premiums

- Cash purchase: No lender requirement for insurance (though still risky)

- Short-term flip: Insurance cost less relevant if holding <1 year

The Bottom Line

Flood zone status is one of the most financially significant factors in property valuation - and one of the most overlooked. A $5,000/year insurance premium over a 10-year hold is $50,000 in carrying costs that need to be reflected in your purchase price.

Always check FEMA flood zone status before trusting any AVM estimate. And when evaluating deals in flood zones, do the math on insurance costs before deciding if it's really a bargain.

AVMLens automatically identifies FEMA flood zones and factors them into geo-risk adjustments. Try it free with 50 tokens.